Zero-rated vs exempt VAT is one of the most confusing topics for UK business owners. Ever wondered why some business deals don’t get taxed while others do? The world of VAT can be confusing, especially when different rules apply to zero-rated and exempt supplies.

It’s key to know the difference between zero-rated and exempt supplies. They might seem the same, but they affect your taxes and finances differently.

In the UK, these terms might seem alike, but they change how you handle taxes. They impact your ability to get back taxes you’ve paid, manage money, and follow HMRC rules. Whether you’re new or big, understanding these can save you money and stress.

This article will clear up the confusion around VAT categories. We’ll share useful tips for better financial choices. We’ll look at key differences, give examples, and warn you about VAT traps.

Ready to improve your VAT knowledge? Let’s dive into the world of VAT and boost your business with expert advice.

Understanding VAT Classifications in the UK

Value Added Tax (VAT) is key for UK businesses. HMRC VAT classifications guide how goods and services are taxed.

The UK’s tax system is complex. Knowing HMRC VAT classifications is vital for your business’s finances and decisions.

The Basics of Value Added Tax

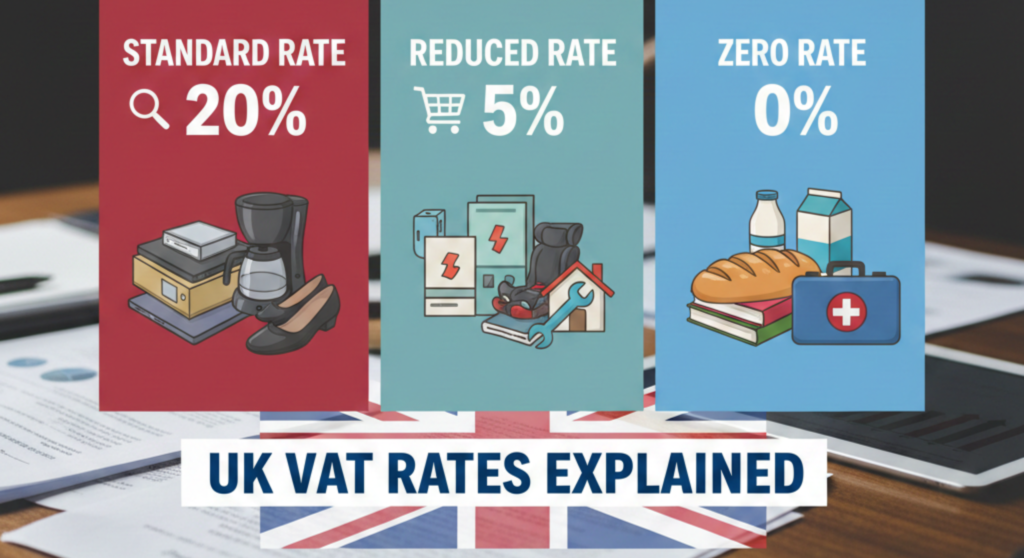

VAT is a tax on most goods and services. Businesses collect tax on sales and get back tax on what they buy. The main VAT rate is 20%, with lower rates for some items.

- Standard rate: 20%

- Reduced rate: 5%

- Zero rate: 0%

Why VAT Classifications Matter for Your Business

Knowing HMRC VAT classifications is crucial. It affects your business in many ways.

- Pricing strategies

- Market competitiveness

- Administrative burdens

- Financial planning

Getting VAT wrong can cost your business a lot. It can lead to fines and cash flow issues. Make sure you classify your products and services correctly.

| VAT Classification | Impact on Business |

|---|---|

| Standard-rated | Full VAT charged at 20% |

| Reduced-rated | Lower VAT at 5% |

| Zero-rated | 0% VAT with input tax recovery |

| Exempt | No VAT charged, no input tax recovery |

Accurate VAT classifications are crucial for your business’s health and HMRC compliance.

What Does Zero-Rated Mean?

Zero-rated supplies in the UK are a special VAT category that affects your business finances. These goods or services are taxed at 0% VAT. This means you don’t charge VAT to customers but can still claim back VAT on business costs.

It’s important for businesses to understand zero-rated supplies in the UK. The government uses zero-rating to make essential items cheaper. It also helps businesses get back VAT on what they spend.

- Zero-rated supplies are charged at 0% VAT

- Businesses can still reclaim input VAT

- These supplies remain taxable for VAT purposes

Key features of zero-rated supplies include:

| Aspect | Details |

|---|---|

| VAT Rate | 0% |

| Input VAT Recovery | Full recovery permitted |

| VAT Registration | May be required if turnover exceeds threshold |

Your business must keep track of zero-rated supplies on VAT returns. Even though you don’t collect VAT, you must keep accurate records. You also need to know which goods and services qualify for this special status.

What Does Exempt Mean in VAT Terms?

Knowing about VAT exempt categories is key for businesses in the UK. VAT exemption changes how companies handle money and taxes.

When a deal is VAT exempt, it’s not taxed like usual. It has its own rules, not a complete tax break.

Key Characteristics of Exempt Supplies

VAT exempt supplies have big effects on businesses:

- No VAT is charged to customers

- No VAT can be reclaimed on purchases related to exempt supplies

- Businesses making only exempt supplies cannot register for VAT

Common Examples of VAT Exempt Categories

Many important areas are VAT exempt:

| Sector | Typical Exempt Services |

|---|---|

| Financial Services | Insurance, loans, credit arrangements |

| Healthcare | Medical treatments, professional health services |

| Education | Courses from recognised educational institutions |

| Property | Residential property sales and long-term lettings |

Grasping these vat exempt categories is vital for businesses. It helps them manage taxes and finances better.

Zero-Rated vs Exempt: The Critical Differences

Understanding vat exemption differences is key for UK businesses. Both zero-rated and exempt supplies seem similar at first. But they have big differences that affect your business’s money plans.

The main vat exemption differences are in several key areas:

- Input Tax Recovery: Zero-rated supplies let you get back all VAT paid on costs. Exempt supplies don’t allow this

- VAT Registration rules are different for each type

- The financial effects are quite different

Zero-rated supplies mean you can get back all VAT on related costs. But exempt supplies limit this, which can raise your costs. This big difference means you need to think carefully about your VAT strategy.

Businesses with zero-rated supplies must register for VAT when they hit a certain amount. But exempt businesses have different rules. They often can’t choose to register. This makes VAT accounting tricky for many companies.

Your business’s situation will decide the best classification for you. Some companies even have a mix of both, making VAT even more complex.

How Zero-Rated and Exempt Status Affect Input Tax Recovery

Understanding input tax recovery is key for businesses dealing with VAT rules. Different VAT types can change how you get back tax on business costs. This affects your company’s money health.

The rules for getting back tax change a lot between zero-rated and exempt supplies. Knowing how these differences affect your tax is important.

Reclaiming VAT on Business Expenses

Getting back input tax depends on your business’s VAT status. For businesses with zero-rated supplies, the tax rules are more flexible:

- Full input tax recovery on business purchases

- Ability to reclaim VAT on goods and services directly related to your business

- Treated similarly to standard-rated VAT supplies

Exempt supplies are harder to deal with. Businesses can’t usually get back input tax on purchases linked to exempt activities. This can make things harder financially.

The Impact on Your Cash Flow

The way you get back input tax can really affect your business’s money flow. Zero-rated businesses get a big advantage because they can recover all input tax, cutting costs. On the other hand, exempt businesses face higher costs since VAT is not recoverable.

Businesses with mixed supplies need to be careful with attribution rules. The de minimis threshold might let them get back some input tax. This can help companies with complex VAT situations.

Planning your finances well is crucial to handle these input tax recovery challenges.

Which Goods and Services Are Zero-Rated in the UK?

Knowing about tax-free goods and services in the UK can really help your business’s finances. Zero-rated supplies have a special VAT status. This means businesses can sell certain items without VAT while still getting back the VAT they paid.

In the UK, there are many tax-free goods and services that get zero-rating. These include:

- Most basic food items for human consumption

- Children’s clothing and footwear

- Books, newspapers, and printed publications

- Public transport services

- Certain construction services for residential buildings

- Domestic water and sewerage services

When it comes to zero-rated supplies, there are certain rules to follow. Not all food items qualify. For example, catering services, hot food, and luxury food products don’t get zero-rating.

Charities often benefit from these zero-rated rules. This lets them use more of their money. Your business can also benefit by sorting out your supplies and following HMRC’s rules.

It’s important to know the difference between zero-rated and exempt supplies. Both have a 0% VAT rate. But, zero-rated items are still taxable. This means you can claim back the VAT you paid.

VAT Registration Requirements for Zero-Rated and Exempt Businesses

Understanding UK VAT thresholds can be tricky for businesses. Knowing when and how to register for VAT is key to following HMRC rules.

Understanding UK VAT Registration Thresholds

The VAT registration threshold in the UK is £85,000. You must consider both zero-rated and standard-rated supplies when calculating your taxable turnover. It’s important to note that exempt business registration is different from standard VAT registration.

- Zero-rated supplies count towards the VAT threshold

- Businesses must register if expected to exceed £85,000 in the next 30 days

- Voluntary registration can be beneficial for reclaiming input tax

When Exempt Business Registration Becomes Essential

Businesses that only offer exempt supplies usually can’t register for VAT. However, there are cases where registration is needed, such as:

- Mixed supplies including taxable and exempt services

- Supplies outside the UK

- Acquiring goods from European Union countries

It’s important to carefully look at your business activities to choose the right VAT registration path. Getting advice from a tax expert can help tailor guidance to your needs.

HMRC VAT Classifications and Compliance

Understanding HMRC’s zero-rated VAT rules is key. Your business needs to keep detailed records. These records must show you follow the UK’s VAT classification system.

There are several important things to know about zero-rated VAT rules:

- Keep detailed records for zero-rated supplies

- Use the right VAT codes in your accounting

- Be ready with accurate info for HMRC checks

- Have solid evidence for zero-rated categories

HMRC has strict rules for reporting zero-rated supplies. You must make sure your VAT returns are correct. Include all the necessary documents for each claim.

Key compliance requirements include:

- Record all transaction details accurately

- Keep invoices and proof of zero-rating

- Have strong internal checks

- Be ready for HMRC investigations

Export-related zero-rated supplies need extra proof. Your documents must show the goods left the UK. They must also meet the zero-rated VAT criteria.

Calculating partial exemption is vital if you handle both taxable and exempt supplies. HMRC needs detailed reports and annual updates. This ensures your VAT accounting is transparent.

Common Mistakes When Applying Zero-Rated VAT Rules

Understanding zero-rated vs exempt VAT can be tricky for businesses. Knowing common mistakes helps you steer clear of costly errors. These errors could lead to penalties from HMRC.

Businesses often make critical errors with VAT classifications:

- Misclassifying supplies between zero-rated and exempt status

- Incorrectly assuming all food products are zero-rated

- Misunderstanding zero-rating conditions for specific services

- Wrongly treating export supplies

Input tax recovery is another area of risk. Exempt businesses might try to reclaim VAT wrongly. Partially exempt organisations face complex apportionment calculations.

| Common Mistake | Potential Consequence |

|---|---|

| Incorrect VAT Classification | Penalties and interest charges |

| Poor Documentation | Rejected VAT claims |

| Registration Errors | Retrospective tax assessments |

Documentation errors can cause big problems. Lack of evidence or missing invoices might attract HMRC’s attention. Businesses need to keep detailed records of their supplies.

Registration mistakes can also be serious. Not registering when you should or registering wrongly can cost a lot of money.

Conclusion

Understanding VAT classifications is key for your business’s financial health. Zero-rated and exempt supplies might seem alike, but they affect your taxes and cash flow differently. Knowing how they impact your tax recovery and business turnover is vital.

Following HMRC rules closely is important. Correctly classifying your supplies can help you stay compliant and save on taxes. If your business deals with complex supplies, getting professional help is a good idea.

VAT classification is not just about following rules; it’s a strategic choice. By grasping these differences, you can make better financial decisions. This could give you an edge over competitors. Always check your supply classifications, keep detailed records, and ask for expert advice when needed.

Managing your VAT status well can bring big financial benefits. Your effort to understand these details can lead to better business operations. It might also help avoid unexpected tax issues in the future.